综合指数 2010年 03月 23日

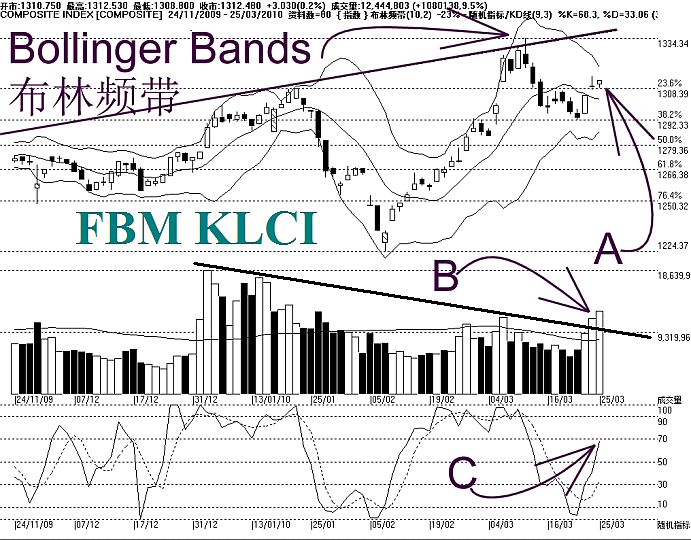

综合指数 2010年 03月 23日富时综合指数周一在1292点的38.2%费氏线上获得扶持后继续回弹,上扬11.20点,以1304.85点闭市,成功的回弹至1300点的心理水平以上。综指当前的阻力水平是1308点的费氏阻力线,支持水平则是1292点的费氏线。

如图所示,综指上探至布林中频带(Bollinger Middle Band)的动态阻力线(参考图中箭头A),惟综指最终仍然受到布林中频带的阻力,未能成功突破。接下来布林中频带继续的成为综指的主要阻力,若综指能上扬突破布林中频带的话,那综指的后市将有望摆脱下跌的窘境。

如图中箭头B所示,虽然马股成交量增长34.5%,这使到成交量成功的超越40天成交量移动平均线(VMA)的水平,这显示整体交投活跃,市场的承接力量也随之增加,这对综指开始转强是有利的。

如图中箭头C所示,随机指标(Stochastic)回弹,这表示综指有望出现技术回弹,无论如何,随机指标还未成功的突破30%,所以综指的短期走势并未完全确定综指出现上扬趋势。换句话说,接下来若随机指标成功突破30%的水平,那综指的短期走势将进入技术反弹的格局。

综指在1292点的费氏线获得支持,由于这也是14、21、31天的加权移动平均线(EMA)的支持点,所以综指回弹。接下来若综指能突破布林中频带,那综指转强的机会将有望提高,届时若能再配合布林频带开始明显打开的话,那综指则有望恢复上扬的趋势。

Composite Index 23/03/2010

Composite Index 23/03/2010

The KLCI rebounded 11.20 points, after being supported by the 38.2% Fibonacci Retracement, and the KLCI closed at 1304.85 points, breaking above the 1300 level. Immediate resistance for the KLCI is at 1308 Fibonacci Retracement while the support is at 1292 Fibonacci Retracement. As indicated by A, the KLCI is testing the Bollinger Middle Band, which is the dynamic resistance. If the KLCI should break above the Bollinger Middle Band, it would break away from the bearish biased short term movement, and there is a better chance of resuming its uptrend.

As indicated by B, total market volume increased 34.5%, breaking above the 40-day VMA level. This suggests that the market participation is now at a healthy level. Generally, if volume should stay above the 40-day VMA level, the market sentiment is likely to improve.

As indicated by C, the Stochastic rebounded, but still has not broken above 30% level. If the Stochastic should break above 30% level, it would be a beginning of a technical rebound for the KLCI.

In conclusion, the KLCI rebounded from 1292 Fibonacci Retracement, which is also the similar level of the 14, 21, 31 EMA. If the KLCI could take out the resistance at the Bollinger Middle Band, the uptrend is likely to resume when the Bollinger Bands should re-expands.

FKLI End Mostly Firmer

FKLI End Mostly Firmer Turnover was lower at 8.704 lots compared to Tuesday's 12,585 lots and open interests slipped to 26,814 contracts from 29,121 contracts before.

Turnover was lower at 8.704 lots compared to Tuesday's 12,585 lots and open interests slipped to 26,814 contracts from 29,121 contracts before.