KL Stock Market May Extend Gains

KL Stock Market May Extend Gains The Malaysian stock market has finished higher now in back-to-back sessions, collecting 8 points or 0.5 percent in the process. The Kuala Lumpur Composite Index finished just above the 1,520-point plateau, and now analysts are forecasting continued support at the opening of trade on Wednesday.

The global forecast for the Asian markets is fairly positive thanks largely to merger-and-acquisition activity. Technology stocks and properties figure to be the key beneficiaries, while gold stocks may fall on profit taking. The European and U.S. markets finished higher on Tuesday, and the Asian bourses also are tipped to track higher.

The KLCI finished slightly higher on Tuesday, nudged into the green by gains from the financial shares, industrial issues and plantation stocks.

For the day, the index added 3.96 points or 0.26 percent to finish at 1,523.37 after trading between 1,518.15 and 1,525.78. Volume was 847.99 million shares worth 1.15 billion ringgit. There were 359 gainers and 344 decliners, with 330 stocks finishing unchanged.

For the day, the index added 3.96 points or 0.26 percent to finish at 1,523.37 after trading between 1,518.15 and 1,525.78. Volume was 847.99 million shares worth 1.15 billion ringgit. There were 359 gainers and 344 decliners, with 330 stocks finishing unchanged.

Among the gainers, Hong Leong Bank, Hong Leong Financial Group, Mclean Technologies, Maybank, CIMB Holdings, Sime Darby and Petronas Chemicals all finished higher.

Hong Leong Bank gained 30 sen to RM11.50 while Hong Leong Financial Group advanced 36 sen to RM11.14. HwangDBS Vickers Research said EON Capital's earnings would be included in Hong Leong Bank's books from today and it expected the assets and liabilities of EON Capital to be vested in Hong Leong Bank on July 1.

"With the stronger balance sheet and greater financial muscle, Hong Leong Bank will be able to look at growth beyond Malaysia to meet its regional aspirations," it said in a research note.

In economic news, Malaysia will on Wednesday announce March figures for industrial production, with forecasts calling for an increase of 3.4 percent on year. That follows the 5.0 percent annual expansion in February.

DJIA 3rd Day Win On Low Volume

DJIA 3rd Day Win On Low VolumeThe lead from Wall Street is optimistic as stocks showed a strong upward move during trading on Tuesday, adding to the gains posted in the previous session and further recovering from last week's losses. The markets benefited from additional merger-and-acquisition activity, with the recent string of multi-billion acquisition agreements seen as a sign of corporate confidence in the economic outlook.

The major averages closed firmly in positive territory, with the NASDAQ just below last Friday's ten-year closing high. The Dow climbed 75.68 points or 0.6 percent to 12,760.36, the NASDAQ rose 28.64 points or 1 percent to 2,871.89 and the S&P 500 advanced 10.87 points or 0.8 percent to 1,357.16.

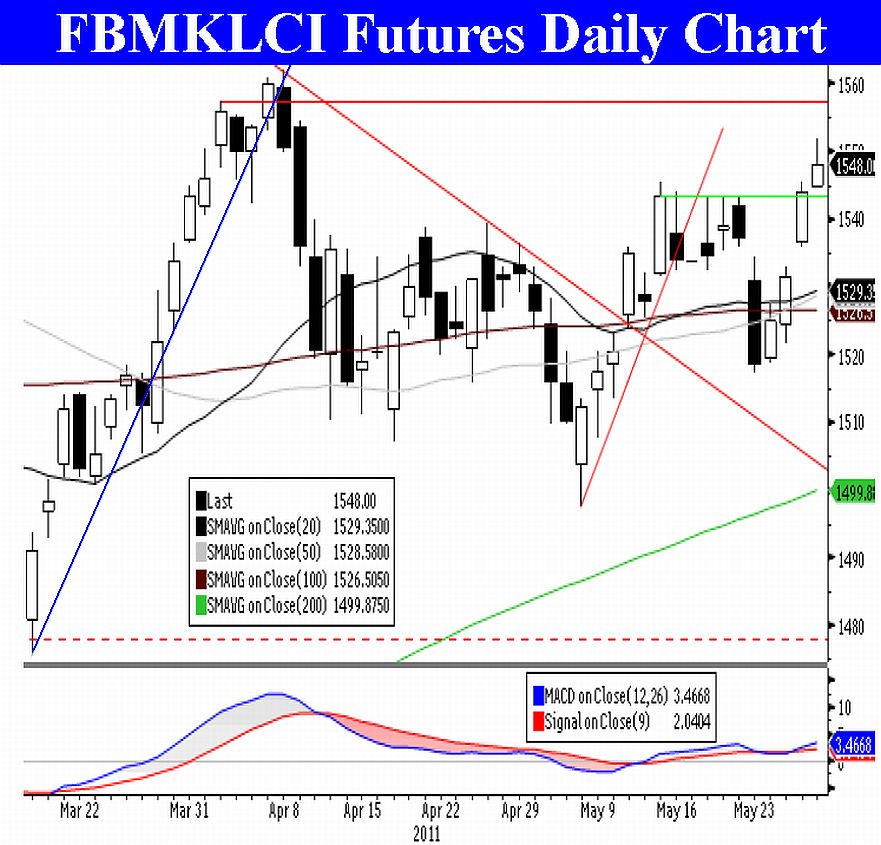

Meanwhile FBM KLCI futures on Bursa Malaysia Derivatives closed higher in line with the cash market. The May and September 2011 rose 3 points to 1,520.5 and 1,519 respectively, June rose 2 points to 1,519 while December stood at 1,512. Volume slipped to 4,637 lots from Monday's 6,939 while open interest was lower at 16,904 contracts from 19,236 previously.

HAPPY TRADING